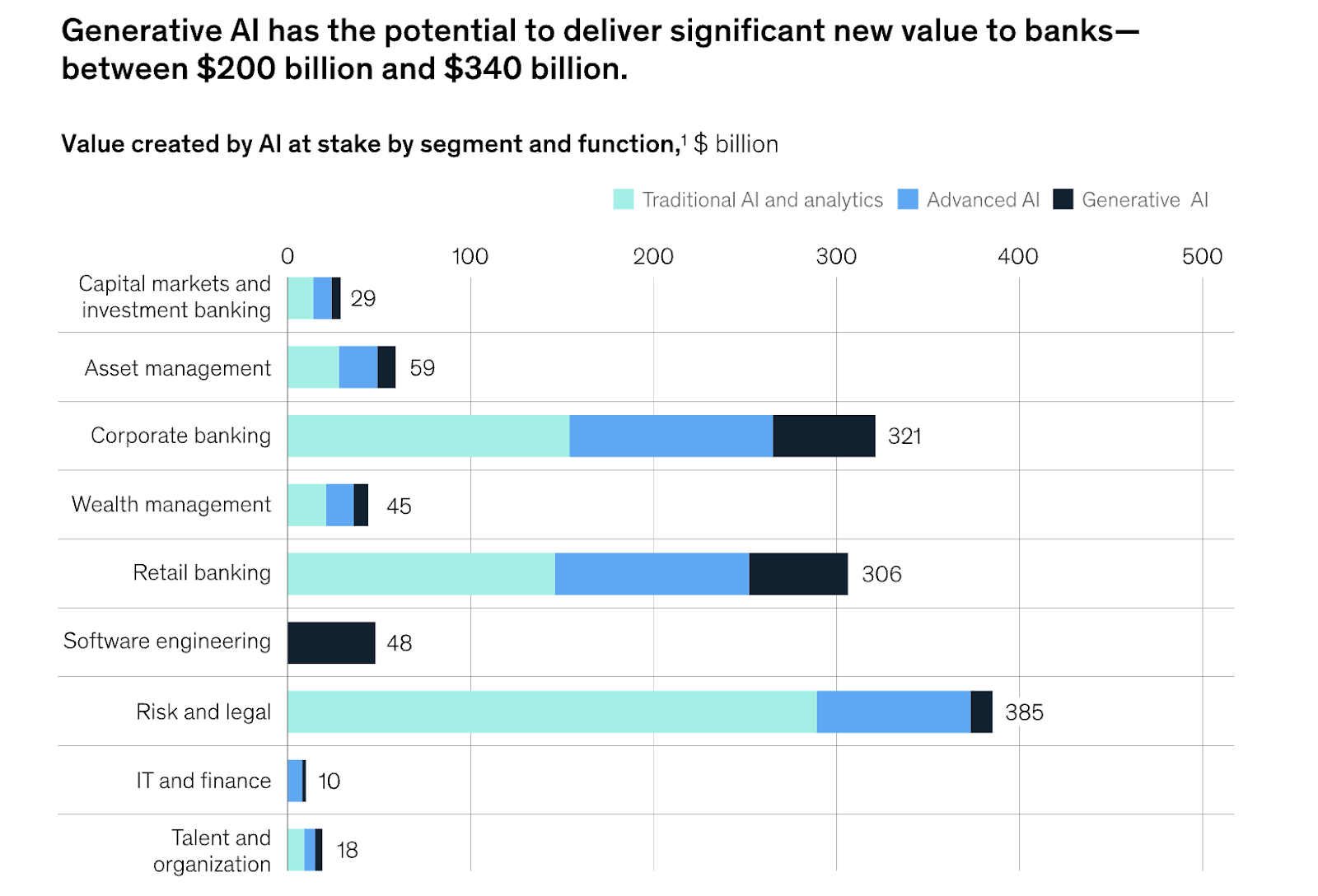

Artificial intelligence, particularly generative AI, is redefining the aggressive fintech landscape.The McKinsey Global Institute recently predicted that generative AI could add an additional $200 to $340 billion in annual value to the banking sector—representing a potential 9-15% uplift in operating profits.

As industry players level up their game, Visa is betting big on AI, releasing over 500 generative AI applications to drive innovation and productivity spike at scale.

The vision for AI integration isn’t just about reducing costs; it’s about redefining workflows. Visa has poured $3.3 billion into AI and data infrastructure over the past decade, most recently channelling $100 million into generative AI startups. The company’s AI-backed credit approval systems even bridge service gaps for banks during network disruptions.

Credit: The McKinsey Global Institute

AI + Humans is the Future

Visa’s approach to AI is less about workforce reduction and more about enhancing human oversight. “My vision is for Visa to have AI-generated digital employees overseen by human workers. Any given human employee can oversee, on average, eight to 10 AI employees that are trusted with a variety of tasks,” said Rajat Taneja, the president of technology at Visa.

Meanwhile, other technology leaders also seem to echo this belief. “I do think there’s a potential to have a high percentage of jobs automated, but I also think there’s a great potential to bring a lot more efficiency to jobs,” said Deb Lindway, executive vice president & head of AI, PNC, in an interview.

BYOT (Bring Your Own Tools)

According to Mckinsey, GenAI comes with plenty of risks, such as misinformation, IP issues, transparency gaps, bias, and security concerns. Sustained value demands moving beyond initial trials and addressing these challenges. It is for this reason that AI at most fintech companies is still largely internal, and not consumer facing.

“We do not have customer-facing use cases. At the moment, all of these cases are internal, and there’s a natural sequence. There have been interesting tales from companies that have gone live with generators and chatbots, and then there have been specified pricing terms that have turned into lawsuits. The legal precedent set is very clear: a customer channel is an extension of the company, and they are accountable for what an AI system generates. Therefore, we want to be very careful before we go live with those,” said Derek Waldron, chief analytics officer at JPMorgan Chase.

Unwilling to play the waiting game, many fintech employees are bringing their own tools to work, even if their companies haven’t officially rolled them out yet. However, caution needs to be exercised here.

“There’s definitely a demand for companies to come up with policies, and come up with ways for these tools to be used because when people just use them rogue, that can create some issues, and can create some inequities,” said Amanda Hoover, senior correspondent at Business Insider, on the need for companies to formally adopt these tools internally to ensure uniformity.

Use Cases of GenAI in Banks

Earlier this year, JP Morgan launched Quest IndexGPT, using GPT-4 to enhance thematic index construction for institutional investors, and introduced LLM Suite, an AI assistant for 60,000 Chase employees to aid tasks like writing emails. Ranked first in the 2024 Evident AI Index, the financial services firm headquartered in New York leads in AI adoption in finance.

Not willing to be left behind, Morgan Stanley launched AI @ Morgan Stanley Debrief around the same time in a bid to boost advisor productivity. It also released the AI @ Morgan Stanley Assistant, adopted by 98% of advisor teams. Jeff McMillan, the head of analytics, data and innovation at Morgan Stanley wealth management and Firmwide AI, describes AI as a window of opportunity. “I’ve never seen anything like this in my career, and I’ve been doing artificial intelligence for 20 years,” he said.

Meanwhile, Visa’s archrival Mastercard has brought in a new AI technology that improves payment security by detecting compromised cards twice as fast and reducing incorrect fraud alerts by 200%. It also identifies at-risk merchants 300% faster, helping spot complex fraud patterns and protect future transactions.

This upgrade strengthens Mastercard’s Cyber Secure program, giving banks and merchants better tools to protect customer data. With faster, more accurate alerts, banks can act quickly to prevent fraud, block compromised cards, and build trust in the payment system.

However, there are areas in finance that are likely to remain AI-proof for a long time to come. “Customer relationships are always going to be high value and irreplaceable. I think finance will always have a very big element of human trust and relationships are going to be very important,” said Derek Waldron, chief analytics officer at JPMorgan Chase, on areas in the financial sector that will win the AI disruption, however, he caveated this with this gap constantly reducing.

GenAI Push in India

In India, AI applications are also transforming banking operations. HDFC Bank, for example, adopted an AI-driven approach to fraud detection, which has proven essential as fraudsters continue to adapt to traditional rule-based systems. In 2017, the bank launched Eva, India’s first AI-driven banking chatbot, handling millions of queries instantly and setting a new standard for customer service.

By 2020, ICICI Bank introduced iPal, enabling transactions via voice commands through Alexa and Google Assistant, but discontinued it in 2021. In 2023, SBI announced an AI initiative to boost decision-making and operational efficiency, planning advanced data systems and fintech partnerships to enhance co-lending.

The post AI is Eating Fintech appeared first on Analytics India Magazine.

{kind=link}