In 2024, NVIDIA had established its long-standing dominance in the sphere of the AI supply chain with advanced GPUs. That was until DeepSeek entered its domain in early 2025, challenging assumptions about scale and rewriting the rules of AI development.

The Chinese lab released a reasoning model that matched or exceeded several Western closed-source systems while training the base model, DeepSeek-V2, on just 2,048 GPUs—far fewer than what frontier labs then used for similar results.

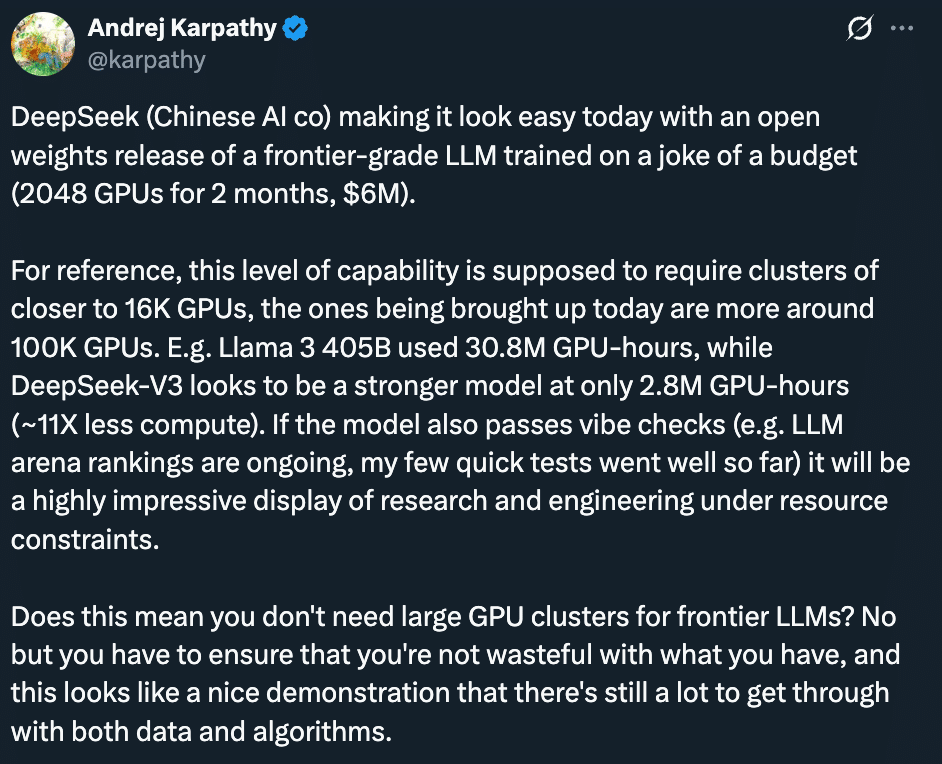

Source: Andrej Karpathy, former OpenAI researcher in a post on X, December 2024.

As attention shifted from sheer compute to architecture, training strategy, and efficiency, NVIDIA’s market capitalisation fell by as much as $600 billion in a single day—the largest such drop for a US company—as investors reassessed the need for ever-larger GPU spending.

Soon, China started deploying DeepSeek across public service platforms and government cloud infrastructure. Universities rolled out customised instances for automated learning assistance, research support, academic planning, and 24/7 student services as part of wider AI-augmented education pilots. Even healthcare, automotive manufacturing, and the military integrated DeepSeek’s LLMs.

The competitive environment pushed US cloud providers to catch up.

Within weeks, AWS added DeepSeek-R1 to its AI services. Microsoft integrated it into Azure AI Foundry and its model catalogue. Google made DeepSeek-R1 available in Vertex AI’s Model Garden, enabling developers to deploy the model within existing cloud workflows.

Over the last year, DeepSeek’s journey has been defined by R1, the absence of its successor, and local rivals taking over.

Usage Patterns and Market Evolution

OpenRouter, a unified API gateway that provides access to hundreds of AI models through a single interface, offers a useful lens on DeepSeek’s adoption. Its routing dataset—covering roughly 100 trillion tokens—shows DeepSeek models accounting for around 14.4 trillion tokens between November 2024 and November 2025.

After the release of DeepSeek V3 and DeepSeek R1, the two together represented more than half of all open-source token traffic on the platform. No other open-weight model family reached comparable concentration during that period.

Pricing played a significant role in the model’s adoption, as DeepSeek consistently ranked among the lowest-cost options for sustained, high-volume routing. But this dominance peaked around mid-2025 and then declined.

OpenRouter’s report identifies a clear summer inflexion.

Source: OpenRouter

There wasn’t a collapse in absolute usage, but a rapid diversification of the Chinese open-source ecosystem. New releases from Qwen, Moonshot AI (Kimi), MiniMax, and others captured production traffic within weeks.

And by late 2025, no single open-source model accounted for more than 20–25% of token share. DeepSeek’s earlier flagpole position declined, giving way to a more pluralistic distribution.

Currently, DeepSeek is going toe-to-toe with other Chinese AI models in absolute benchmarks. But it is in no hurry to recapture the throne.

The Research Focus

Rather than accelerating product releases like Western AI labs and Chinese rivals, DeepSeek pivoted towards research, training methods, and infrastructure.

Post-R1, DeepSeek focused on exploring the nitty-gritty details of an LLM’s architecture and incrementally fixing bottlenecks that hampered compute efficiency. This was in line with the struggles the country faced due to export restrictions the US government placed on NVIDIA for selling GPUs to a Chinese tech company.

In February 2025, with a five-day open-source initiative, DeepSeek released frameworks focused on execution efficiency, pipeline scheduling, core computation, parallel workload coordination, and large-scale storage. These addressed the bottlenecks that determine whether models can be trained and served cheaply at scale, and were aimed squarely at production engineers.

Throughout the year, the DeepSeek-R1 also received incremental updates that boosted its performance on benchmarks, and the company also ran numerous research works and experiments on the base model, the DeepSeek-V3.

Notably, in September, DeepSeek released V3.2-Exp, an experimental model designed to push long-context capabilities while keeping efficiency central, with 3.5x lower prefill costs and up to 10x cheaper decoding during inference for a 128k context window.

In October, it released DeepSeek-OCR. The model converts text into compact visual tokens, enabling compression ratios of 9–10x with over 96% precision, and around 60% accuracy even at 20xcompression. The work suggested a new efficiency path in which visual modalities are used not for perception but for memory and context optimisation in language models.

And, in November, it published research on a model that achieved gold-medal-level performance at the International Math Olympiad 2025. It became the only company to achieve the status after OpenAI and Google DeepMind. This model, the DeepSeek-Math-v2, addressed a growing concern in reasoning and math benchmarks, namely that many models arrive at correct answers without sound or inspectable reasoning.

What Next?

A recent Microsoft report showed DeepSeek achieving significant market penetration outside China, with about 43% usage in Russia and roughly 56% in Belarus, making these among the highest adoption rates globally. In China, DeepSeek’s share of generative AI usage is approximately 89%.

Source: Microsoft

By contrast, adoption in Western Europe and North America remains low, often under 5%. In many African countries, usage is 2–4 times higher than in Western Europe or North America, driven by DeepSeek’s free or low-cost access with minimal subscription barriers, which makes it appealing in price-sensitive markets where Western alternatives are less accessible.

With growth concentrated in developing regions, how DeepSeek adapts its future models and services to meet these markets’ specific needs will be an important indicator of its global strategy.

However, the lack of a successor to its R1 model is noteworthy.

According to a Reuters report in mid-2025, DeepSeek did not release the expected DeepSeek R2 at the anticipated time because the company’s leadership, including founder Liang Wenfeng, was not satisfied with the model’s performance and stability, pushing its launch beyond the originally planned May 2025 date.

Additional factors included slow data labelling, technical problems tied to hardware choices (such as instability and connectivity issues with Huawei chips that DeepSeek had been encouraged to adopt), which forced the company to prioritise stability by sticking with NVIDIA GPUs for training and using those other chips only for inference.

Now, DeepSeek is planning to launch a new base model, DeepSeek-v4, with a clear emphasis on coding and math performance, according to The Information. But this time, it will not have the first mover’s advantage in the open-source ecosystem.

The post DeepSeek’s Rise, Pause, and How Local Competition Took Over appeared first on Analytics India Magazine.